ER Portfolio Allocation - April 2006

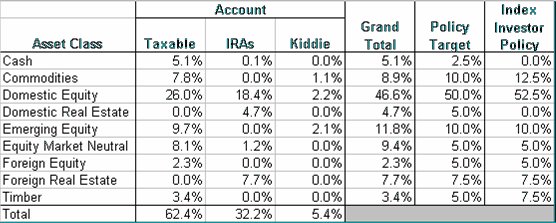

Here's my latest asset allocation (click for a larger image)...

Not too different from my March allocation... I did reduce my cash position from 5.1% down to 2.1% by purchasing EFV (Foreign Value Index) and EWU (UK Index). This move also brought by foreign equity position from 2.3% up to 4.9% - close to my policy target.

I am still a bit overweight in Emerging Equity and I'll probably end up selling AUO (an Emerging Equity Prudent Speculator pick) this coming month. I've got a 32% return and I really have no business owning any single emerging equity stock.

I'll be compiling my portfolio performance this weekend and I'm guessing April will be another good month.

posted by Early Riser @ 8:09 AM

0 comments

![]()

![]()